Voice and SMS revenues are declining dramatically for communications service providers (CSP). Telco 2.0 expects SMS revenues in Europe and the Middle East to drop 40 percent by 2015, while Strategy Analytics predicts that CSPs around the world will lose about $3 billion in revenue between 2012 and 2017.

And where’s all the money going? To over-the-top (OTT) providers that offer consumers third-party ways of messaging. Apple, Facebook, Skype and WhatsApp are just some of the players in the space. OTT messaging just keeps getting more popular, too. By the end of 2013, Informa Telecoms & Media estimates that OTT messages will be double the number of peer-to-peer SMS messages.

Neutralising the Threat

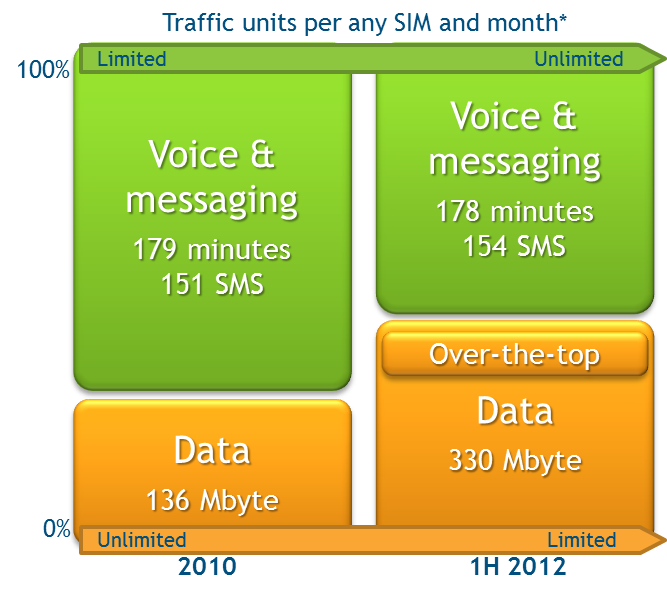

One trend that has seen some adoption has been the shift to reversed, limited to unlimited bundles. International telco efficiency specialist, tefficient recognized that between 2010 and 2012 as data demand showed significant growth, the OTT monetization opportunity had increased.

At the same time, operators started to reverse their mobile bundle offerings in terms of voice and data. The studyrevealed that instead of packaging limited voice minutes and SMS with unlimited data, operators increasingly limited the amount of inclusive data while making voice and SMS unlimited. Of course this has the effect to neutralise the OTT threat and supporting the opportunity for operators and OTT’s to partner.

CSPs remain understandably worried about this new competition, but most aren’t sure how they can solve the problem. Yet one Australian operator, Telstra Global, has a solution: improve the customer experience and bundle services.

Competing Directly with OTT Services

A good number of CSPs have been trying to quietly ignore OTT providers, because they’re not quite sure where to start when it comes to developing a competing solution. Telstra Global has discovered that it’s just a matter of building the right service packages and the right partnerships.

Martijn Blanken, managing director, told Total Telecom that there is “a way to beat” OTT services like WhatsApp, and it comes down to packaging things differently. That’s how Telstra Global has been able to protect SMS revenues as the technology evolves. Blanken noted, too, that OTT providers need the connectivity and network power that CSPs can offer, which can pave the way for strategic alliances that can benefit everyone.

More than anything, however, Blanken emphasised customer service. “The true differentiation will be the customer experience,” he told the news outlet, and everyone from every department will have to be involved.

Packaging Services in a Way that Works

We’ve long believed the same thing – these days, customers are looking for the best possible experience from their CSPs. Research from Vanson Bourne shows that nine out of ten consumers want more personalised interactions with their mobile operators. The advantage that traditional mobile operators have over OTT services is that they know their customers already. It’s just a matter of leveraging big data analytics to create an individual experience for each customer.

If CSPs could use technology like predictive analytics to anticipate mobile habits, then it would be possible to create unique service packages that are superior to OTT models. Automatically sending a customer a relevant solution delivers a great experience that he or she is very likely to remember. As personalisation becomes the norm for customer service, big data analytics will allow CSPs to create new revenue streams and, best of all, work with OTT services to deliver next-generation customer experiences.

At Management World 2013 in Nice, France, Keith Willets, the chairman of TM Forum, highlighted something that’s on the mind of every communications service provider (CSP): declining revenues. A lot of this decline isn’t from competition and certainly isn’t from a lack of demand, either. It’s from the radical changes in mobile usage habits around the world.

The drastic decline in SMS, amounting to about $30 billion in lost revenue last year, is one example that Willets mentioned. The text message is swiftly being replaced by IP-driven services like iMessage, leaving no room for CSPs to build new opportunities in the same space. Instead, as Willets explained, they need to look elsewhere.

The Customer Conundrum

Amid the panicking about changing consumer habits, there’s something even more important that’s fallen to the wayside: the consumers themselves. The telecommunications industry has six billion customers around the world, and Willets reminded everyone at Management World 2013 that telco is ranked in the lowest quartile for customer experience.

Changing the way CSPs interact with customers was part of Willets’s survival kit for this “digital storm.” He listed data analytics, real-time offers and bundles as being critical for operators to build a sustainable business and better relationships with customers.

Willets’ point was simple: if CSPs treat their customers well, they’ll be more tolerant and forgiving. In a world where CSPs are scrambling to create new revenue streams, the customer has to stay top-of-mind.

Overcoming the Paradox with Personalisation

What I heard from Willets’s speech was everything that Comptel has been working on. With traditional sources of revenue declining steeply, CSPs have to recalibrate by focusing on personal, customised offers that serve to engage, delight and sell to customers at the same time.

Predictive analytics should be at the core of this approach. If CSPs can use big data to hone in on customers’ behaviours and needs—and automatically and proactively leverage that knowledge for new business opportunities—then this era of sweeping change across the telco industry will clearly be change for the better.

Considerations for a Next Generation of Mediation – Balancing the Data Explosion with Revenue Monetisation

We’ve often discussed and debated the negative “scissor effect” phenomenon that operators are facing today when it comes to data services. In a nutshell, it’s the inverse relationship between growth in data traffic and decline in operators’ revenue.

There are several key factors that will drive data service growth in the coming years, which are contributing to broadening the gap, typically an improvement in network performance and growth in video services, growth in M2M-based business modelsandthemove toward service convergence.

On a positive note, operators do not have a lack of data when it comes to subscribers, their usage transactions, network performance, cell-site information, device-level data, as well as data spread across their networks and back office systems. But will they have the innovation, know-how and drive to stitch the two together (data growth + subscriber & service awareness) to bridge the chasm being formed by declining revenues?

Often unappreciated, never given enough due but playing a pivotal role in the context of operator revenue monetisation strategies are next-generation data mediation platforms. These platforms will provide operators with the foundation to achieve true convergence and increase service velocity byrapidly introducing next-generation services and launching IP-based services that dramatically increase transactional volumes.

Old-fashioned, batch-oriented mediation platforms are gradually becoming archaic, and the need of the hour is real-time, scalable, flexible, network-driven, bi-directional, on-line and offline charging mediation platforms.

Scalability, processing performance and the ability to run on low-cost hardware are some of the key challenges that must also be addressed by these next-generation data mediation systems. In fact, next-generation data mediation platforms need a multitude of evolved and new capabilities ranging from being network, technology and vendor-agnostic, to supporting triggering and analytics.

Comptel Convergent Mediation supports system consolidation and mediation of all services through a total cost of ownership (TCO)-sensitive, single-platform approach. Regardless of whether end customers are prepaid or postpaid, it enables differentiation in highly competitive markets by offering a smooth evolution of the current network—and accompanying OSS/BSS environment—into a fully convergent solution, with best-of-breed, field-proven modules.

This blog post is based upon a recent Comptel-commissioned Heavy Reading whitepaper, “Balancing Act: Data Explosion vs. Revenue Monetisation – Considerations for a Next Generation of Mediation”. Comptel would like to acknowledge Heavy Reading senior analyst Ari Banerjee for his role in the development of the content.

Last month, Comptel and partners Cisco and Alcatel-Lucent led an interactive session at the Comptel User Group (CUG). (We also captured snapshots of it, as well as some of the presentations and attendee testimonials, in the following video.)

During the interactive session, we polled the approximately 100 telecom executives in attendance on their perceptions of new technologies, like cloud, LTE, M2M and third-party applications, and the consequential impact on communications service providers’ (CSPs) business models. After analysing the data, we wanted to share some of the interesting survey findings.

Nearly 60% of attendees considered LTE-enabled mobile broadband to hold the greatest potential for transforming CSP revenue models over the next 18 months. Interestingly, both the Cisco and Alcatel-Lucent representatives on the panel, when asked to comment, said that they see cloud and mobile data applications as the killer revenue drivers.

Meanwhile, some OSS/BSS industry analysts, like Teresa Cottam of Telesperience, made the point that the responses would be different if the CUG attendees were asked about the next 36 months.

So, we ran the vote again and saw that responses were much more fragmented; a third selected third-party applications and content, a little more than a quarter chose LTE-enabled mobile broadband, and only a share of votes went to M2M and cloud.

The conclusion from the panel and from other commentators was that LTE will lay the grounds for new business models, hence the short term (18 months) bet on it and the longer term belief in cloud, content and M2M.

Other feedback to the CUG survey revealed that:

In terms of revenue erosion, 60% of attendees thought that LTE-enabled mobile broadband will significantly wear down the revenues of fixed-line businesses, while 40% of respondents said that the impact would be marginal.

Three-quarters of respondents mentioned that they are either already working with third-party application and content providers (ACPs) or are planning to within the next 12 months. All respondents expected CSPs to be working with third-party ACPs within the next three to five years.

Finally, 97% of CUG attendees responded that cloud services will definitely generate revenues, but only 22% noted that these will be significant for CSPs. Most (59%) concluded that cloud services will result in relatively modest revenues for CSPs.

Overall, operators seem to be optimistic about the impact of new technologies but are unsure as to how these will translate into new revenue streams.

We’d love to hear your thoughts on the CUG poll results—do you agree or disagree with any of the findings?

{kind=link}

{kind=link}